The Autotransfusion Systems Market is a mature but evolving segment of perioperative blood management

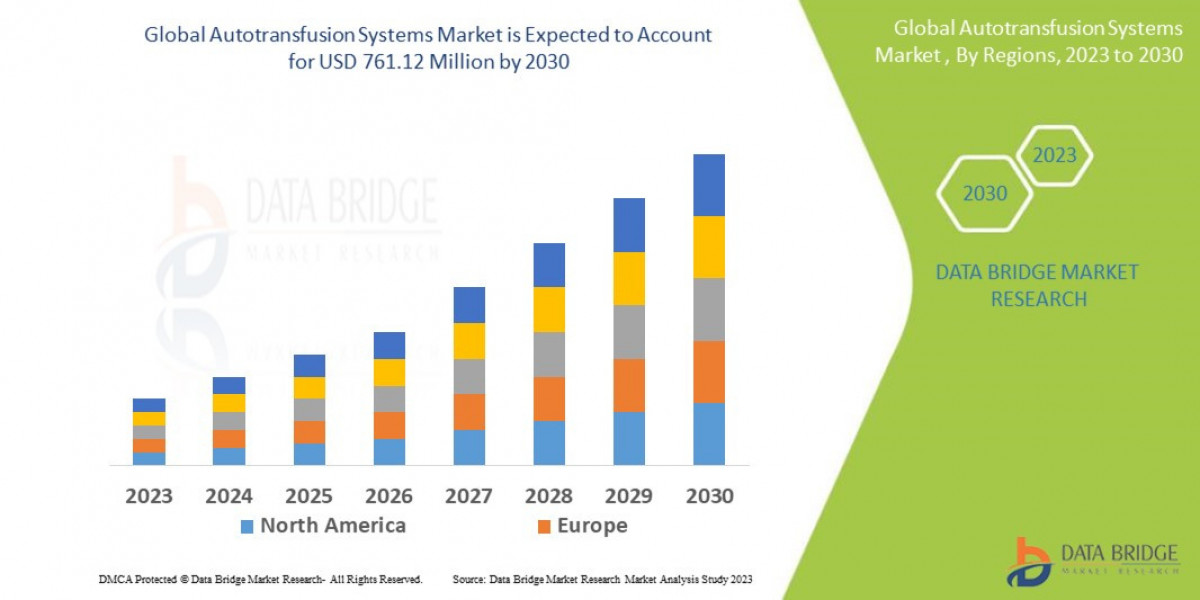

driven by rising surgical volumes, an emphasis on patient blood management (PBM), and technology upgrades in autotransfusion devices and consumables. Data Bridge Market Research has quantified a baseline market valuation and a pragmatic growth trajectory — benchmarking the market at USD 492.20 million in 2022 with a forecast to reach USD 761.12 million by 2030 at a 5.6% CAGR (2023–2030).

(Databridge report link shown above; Databridge report company overview is available separately: Databridge — Autotransfusion Systems Market (Companies).)

Market Overview

Autotransfusion systems (intraoperative and postoperative devices that recover and re-infuse a patient's own blood) reduce dependence on allogeneic blood, lower transfusion-related risks, and align with regulatory and institutional directives around PBM. Key value drivers include: improved device automation, higher-efficiency blood washing/filtration, single-use consumables optimization, and integration with hospital blood-management protocols.

Market Size & Forecast

Multiple authoritative sources converge on a steady mid-single-digit CAGR for the autotransfusion market. Data Bridge estimates the market at USD 492.20M (2022), growing to USD 761.12M by 2030 — CAGR 5.6% (2023–2030).

Independent market intelligence providers report comparable trajectories (for context): Grand View Research and Market Insights sources indicate a market base near the USD 480M–520M range in the early 2020s with expected CAGR results between ~5%–6.5% through the early 2030s, resulting in 2030–2032 market sizes in the USD 500M–910M band depending on methodology.

Practical planning assumption for strategic decision-making: adopt the Databridge mid-case (5.6% CAGR to 2030) for near-term capacity and R&D planning, while modeling upside scenarios (6.0%–7.5% CAGR) for aggressive go-to-market strategies and new product launches.

Market Segmentation

By Product Type

- Standalone Autotransfusion Devices (cell salvage machines: intraoperative, postoperative, dual-mode)

- Consumables & Accessories (collection reservoirs, centrifuge bowls, filters, tubing sets)

- Services & Maintenance (training, validation, clinical support)

By Application

- Cardiovascular Surgery (CABG, valve procedures)

- Orthopedic Surgery (THA, TKA)

- Trauma & Emergency Surgery

- Transplantation & Major Abdominal Procedures

- Obstetrics (selected high-risk cases)

By End-User

- Hospitals (tertiary, academic medical centers)

- Ambulatory Surgery Centers (ASCs)

- Trauma Centers & Military Field Hospitals

- Specialty Clinics & Research Institutions

By Distribution Channel

- Direct hospital contracts / OEM direct sales

- Medical device distributors & group purchasing organizations (GPOs)

- Value-added resellers (service + consumables bundles)

Regional Insights

North America leads by revenue and adoption due to high surgical volumes, established PBM programs, and reimbursement frameworks that support autotransfusion adoption. Europe is a close second, driven by cardiac and orthopedic procedure volumes in Germany, UK, France, and the Nordic markets. Asia–Pacific is the fastest-growing region (adoption acceleration in China, India, Japan) as hospital capacity expands and procedural access increases. Emerging markets in Latin America and Middle East & Africa show selective adoption based on hospital tier and trauma-care investment.

These regional dynamics are consistent across multiple analyses and should inform prioritized commercial investments (e.g., field clinical support and consumables stocking in North America/EU; training and price-sensitive SKUs for APAC).

Competitive Landscape

The autotransfusion systems market is consolidated around established medtech players and a set of regional specialists. Market leaders and notable active players include:

- Haemonetics Corporation — comprehensive blood management portfolio (cell salvage & disposables).

- Terumo BCT — autotransfusion products and global distribution footprint.

- Medtronic — surgical systems portfolio and strategic partnerships.

- Fresenius Kabi — consumables focus and hospital channel leverage.

- Zimmer Biomet / Armstrong Medical — orthopedic-centric adoption and consumable supply models.

- Becton, Dickinson and Company (BD) — peripheral blood management and procedural consumables.

For an industry-curated list of companies covered by Data Bridge in their autotransfusion report, see the Databridge companies page referenced in the Executive Summary. Strategic M&A, OEM-distributor alliances, and consumables-as-recurring-revenue plays define current competitive moves.

Trends & Opportunities

- Consumables recurring revenue: focus on disposable tubing/filters creates long-term annuity streams — commercialize bundled device + consumables agreements.

- Integration with PBM workflows: software-enabled analytics for intraoperative blood loss tracking and compliance reporting.

- Miniaturization & ease-of-use: compact systems for ASCs and frontline trauma units to unlock new end-user segments.

- Cost arbitrage in emerging markets: lower-cost device variants and validated reprocessing programs expand addressable markets.

- Clinical evidence & guideline adoption: invest in outcomes studies that demonstrate reduced allogeneic transfusion rates and total cost of care benefits.

Challenges & Barriers

- Price sensitivity: capital cost of devices and recurring consumables can slow procurement in price-constrained hospitals.

- Reimbursement variability: inconsistent reimbursement frameworks across geographies impede uniform adoption.

- Clinical inertia: entrenched allogeneic transfusion practices and lack of clinician training can limit uptake.

- Regulatory & validation burden: device approvals, sterilization/validation of disposables, and hospital credentialing are time-consuming and costly.

- Supply chain for disposables: reliable supply of single-use components is mission-critical and a potential bottleneck during global disruptions.

Conclusion

The Autotransfusion Systems Market represents a strategically important and financially resilient segment within surgical blood management. Conservative market modeling per Data Bridge projects steady expansion to USD 761.12M by 2030 (CAGR 5.6%), while alternative intelligence providers suggest upside scenarios depending on regional adoption, pricing models, and consumable monetization strategies. Decision-makers should prioritize consumables recurring-revenue models, PBM clinical partnerships, and APAC commercialization to capture the next wave of growth. :contentReference[oaicite:4]{index=4}

Browse Trending Report:

Global Hydrotreating Catalysts Market

Global Industrial Hoses and Fittings Market

Global Internet of Things (IoT) Telecom Services Market

Global Jojoba Oil Market

Global Limestone Market

Global Malware Analysis Market

Global 2-Methyl-4-Chlorophenoxyacetic Acid (MCPA) Pesticide Market

Global Microvascular Angiopathy Treatment Market

Global Mulch Films Market

Global Multiplex Testing Market

Global Nasal Polyps Treatment Market

Global Neonatal Jaundice Management Market

Global Neurorehabilitation Devices Market

Global Nucleic Acid Amplification Market

Global Oligonucleotide Synthesis Market

Contact Us

Data Bridge Market Research

For custom enterprise intelligence, market entry playbooks, or competitor landscaping, engage Data Bridge for bespoke deliverables and clinical evidence mapping.

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email: corporatesales@databridgemarketresearch.com