Market Overview:

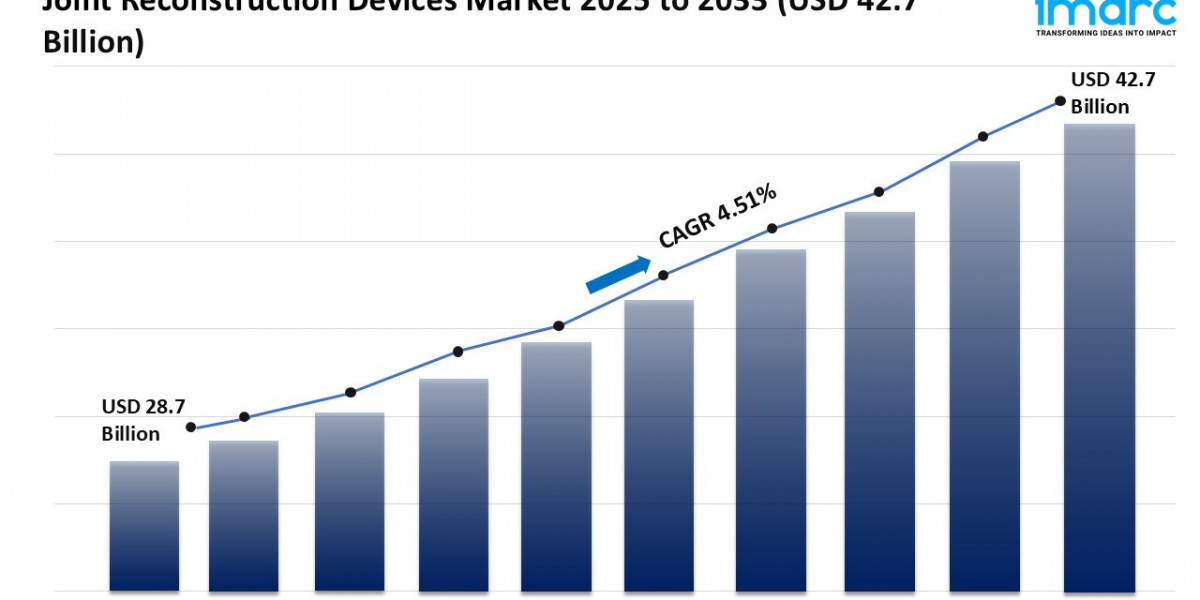

The joint reconstruction devices market is experiencing rapid growth, driven by increasing global geriatric population, rising prevalence of musculoskeletal and orthopedic disorders, and technological advancements in surgical techniques and implants. According to IMARC Group's latest research publication, "Joint Reconstruction Devices Market Size, Share, Trends and Forecast by Technique, Joint Type, End User, and Region, 2025-2033", offers a comprehensive analysis of the industry, which comprises insights on the global joint reconstruction devices market share. The global market size was valued at USD 28.72 Billion in 2024. The market is projected to reach USD 42.72 Billion by 2033, exhibiting a CAGR of 4.51% from 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/joint-reconstruction-devices-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Joint Reconstruction Devices Market

- Increasing Global Geriatric Population

The demographic shift toward an aging population worldwide is a primary catalyst for the joint reconstruction devices market. As individuals live longer, the cumulative wear and tear on joints significantly increases the incidence of age-related joint conditions, particularly osteoarthritis and rheumatoid arthritis. This patient pool inherently drives demand for restorative surgical procedures like total knee and hip replacements. For instance, in 2024, the global market for joint reconstruction devices was valued at approximately $28.7 billion, with the substantial and growing segment of elderly patients being a crucial consumer of these devices. This factor is especially potent in developed regions, such as North America, which held a significant market share—about 46% in 2024—largely due to a mature and aging populace seeking to maintain an active, high-quality life through joint replacement.

- Rising Prevalence of Musculoskeletal and Orthopedic Disorders

A significant rise in conditions like osteoarthritis, which causes joint pain and stiffness, directly correlates with the growing demand for joint reconstruction devices. Lifestyle factors such as rising obesity rates, which place excessive stress on load-bearing joints like the knee and hip, accelerate joint degeneration. Furthermore, the global increase in sports-related injuries and trauma cases resulting from road traffic accidents contributes to the need for surgical repair and replacement. For example, reports indicate that over 350 million people worldwide are affected by arthritis, underscoring the massive patient base. This high prevalence is driving major industry players like Zimmer Biomet and Stryker to continually introduce new implant designs and materials to meet the escalating clinical need.

- Technological Advancements in Surgical Techniques and Implants

Continuous innovation in medical technology has revolutionized joint reconstruction, making procedures safer, more precise, and more effective, which in turn encourages patient acceptance and surgical adoption. The development of advanced, emerging technologies such as robotic-assisted surgery and 3D printing is enhancing procedural accuracy and patient outcomes. For instance, the knee replacement segment accounted for approximately 45.45% of total revenue in 2024, a dominance partly attributed to the integration of these technologies. Robotic systems assist surgeons with meticulous component positioning, while 3D printing facilitates the creation of patient-specific, customized implants, addressing unique anatomical needs. This technological push is a crucial market driver, as evidenced by recent regulatory approvals for advanced systems like the VELYS Robotic-Assisted Solution.

Key Trends in the Joint Reconstruction Devices Market

- Adoption of Robotics and Navigation Systems

The integration of robotic and computer-assisted navigation systems is rapidly moving from a novelty to a standard of care in major orthopedic procedures like hip and knee replacement. This trend is driven by the demonstrated ability of these systems to improve surgical precision, leading to better long-term implant longevity and function. Companies such as Stryker, with its Mako system, and DePuy Synthes are heavily investing in this technology. Real-world application shows that these systems allow for enhanced component alignment and more accurate soft tissue balancing, which are critical factors in reducing the need for revision surgeries. The focus on improved patient outcomes and the push for value-based care models are accelerating the adoption of these sophisticated digital tools in hospitals and ambulatory surgical centers globally.

- Shift Towards Outpatient and Ambulatory Surgical Centers (ASCs)

There is a pronounced market trend toward performing joint replacement procedures, particularly total knee and hip replacements, in ambulatory surgical centers (ASCs) rather than traditional inpatient hospital settings. This shift is primarily fueled by the desire for reduced healthcare costs and a patient preference for faster recovery in a non-hospital environment. Modern surgical protocols, including minimally invasive techniques and superior pain management, have made same-day discharge feasible and safer for a large portion of the patient population. Consequently, the demand for joint reconstruction devices that are compatible with these streamlined, high-volume outpatient settings is increasing, promoting the development of efficient surgical workflows and implant systems that facilitate rapid rehabilitation.

- Customization and Patient-Specific Implants

The market is increasingly embracing the development of patient-specific instrumentation and custom-made implants, moving away from a 'one-size-fits-all' approach. Leveraging technologies such as medical imaging and 3D printing, manufacturers can now design and produce implants that are perfectly tailored to an individual patient's anatomy, accounting for unique bone morphology and joint mechanics. For example, some companies offer personalized instrumentation guides that map out the cuts and placement of the implant before the procedure, dramatically enhancing accuracy. This trend reduces operative time, minimizes bone resection, and is linked to better functional outcomes and patient satisfaction by ensuring a better fit. This bespoke approach is particularly gaining traction in complex revision surgeries or for patients with highly deformed joints.

Leading Companies Operating in the GlobalJoint Reconstruction Devices Industry:

- Allegra

- Conformis

- Conmed Corporation

- Enovis

- Exactech Inc.

- KYOCERA Medical Technologies, Inc.

- Medacta International SA

- Medical Device Business Services, Inc. (Johnson & Johnson)

- MicroPort Orthopedics, Inc.

- Smith & Nephew

- Zimmer Biomet

Joint Reconstruction Devices Market Report Segmentation:

By Technique:

- Joint Replacement

- Implants

- Bone Graft

- Osteotomy

- Arthroscopy

- Resurfacing

- Arthrodesis

- Others

Joint replacement leads the market with a 52.34% share in 2024, driven by its effectiveness in restoring mobility and alleviating pain through advanced, durable implants and less invasive methods.

By Joint Type:

- Knee

- Hip

- Shoulder

- Ankle

- Others

Knee reconstruction holds a 45.45% market share, as it addresses frequent wear and tear and degenerative issues, enhanced by improved implant designs and a focus on mobility preservation.

By End User:

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers (ASCs)

- Others

Hospitals are the largest end-user segment, providing comprehensive orthopedic care with advanced facilities and experienced surgeons for various joint reconstruction procedures.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the joint reconstruction devices market with a 45.8% share, supported by a robust healthcare infrastructure, advanced technologies, and a strong emphasis on mobility and recovery.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302