Market Overview

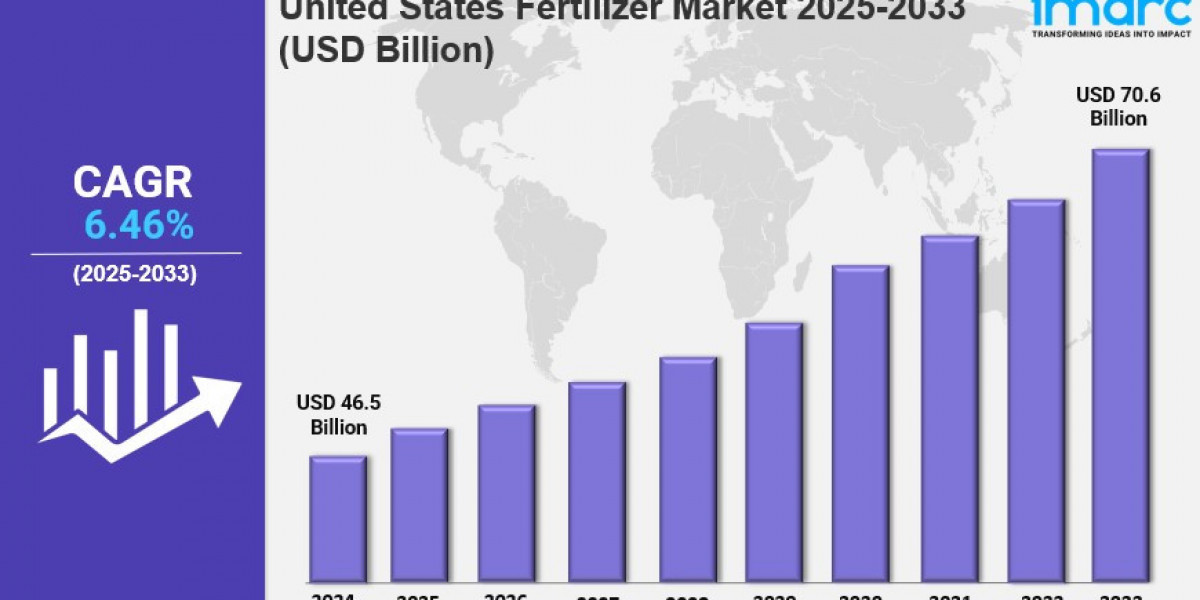

The United States fertilizer market was valued at USD 46.5 Billion in 2024 and is projected to reach USD 70.6 Billion by 2033, growing at a CAGR of 6.46% during the forecast period of 2025-2033. Growth is driven by high agricultural productivity demands, advancements in fertilizer formulation technologies, and widespread adoption of precision farming. Key market segments include chemical and dry fertilizers, with grains and cereals as major consumers due to their extensive cultivation and nutrient needs.

Study Assumption Years

● Base Year: 2024

● Historical Year/Period: 2019-2024

● Forecast Year/Period: 2025-2033

United States Fertilizer Market Key Takeaways

● Current Market Size: USD 46.5 Billion in 2024

● CAGR: 6.46% from 2025 to 2033

● Forecast Period: 2025-2033

● Precision farming and sustainable farming are transforming fertilizer usage, with organic and bio-based products gaining traction.

● Government incentives, increased crop yields demand, and improved soil awareness drive market growth.

● Challenges include variable input prices, environmental concerns, regulatory pressure, and supply chain disruptions.

● Opportunities lie in green fertilizers, digital farming technologies, and local production enhancement.

● Growing demand for nutrient-enriched soils due to biofuel sector expansion boosts the market.

Sample Request Link: https://www.imarcgroup.com/united-states-fertilizer-market/requestsample

Market Growth Factors

Demand for fertilizer in the US is expected to increase along with the rising demand to produce more food to meet the needs of a growing population. According to the US Census Bureau, the population of the US grew by around 1% to reach 340.1 million in 2024 in accordance with estimates, which is higher than the annual average population growth rate since 2000. Fertilizer use rises to maintain fertile soil. Bio-based fertilizers and controlled-release fertilizers make use more efficient for the user. Bio-based fertilizers in conjunction with controlled-release fertilizers reduce environmental impacts because their use minimizes nutrient losses with a gradual release of nutrients. Government initiatives encourage farmers to use modern fertilizers for improved yields. These initiatives also reduce wastage. The reason is that these initiatives promote balanced nutrient management and precision farming.

The expansion of biofuel production, including feedstock crops like soybeans and corn, is also driving demand. In January 2024, the U.S. Energy Information Administration stated that renewable diesel and biofuel could produce 4.3 billion gallons each year with a measurement of 1.3 billion gallons more than in January 2023. Other market demands driving the fertilizer market are fuel ethanol consumption and the degradation of the soil. Fuel ethanol is mixed in gasoline and is produced using corn kernels. Climate varies and creates demand for specialized fertilizers that minimize how soil degrades crops. Specialty and organic fertilizers have demand because people prefer sustainable products as companies research and develop new fertilizer technologies.

The United States fertilizer market demand is expected to benefit from recent technological advancements and supportive agricultural policies, driven by growing investments in precision farming, smart nutrient management, and sustainable agricultural practices aimed at enhancing productivity and environmental efficiency. These are aimed toward improving fertilizer application efficiency and minimizing environmental runoff. Specialty fertilizers, including slow-release fertilizers, micro-nutrients, and water-soluble fertilizers, can meet high-value crop nutrition needs, allow achievement for sustainability objectives, and make optimal yield quality within crops such as nuts, fruits, and vegetables. These technologies such as GPS mapping and soil sensors receive wide adoption by farmers. This enables farmers to accurately manage application of nutrients to reduce over-usage. This combination of factors is driving market growth within the United States.

Market Segmentation

By Product Type:

● Chemical Fertilizer: Dominates with around 98.9% market share in 2024, offering nutrient enhancements for large-scale farming through nitrogen, phosphorus, and potassium formulations.

● Biofertilizers: Noted as a segment but specific market share not provided.

By Product:

● Straight Fertilizers:

● Nitrogenous Fertilizers: Includes urea, calcium ammonium nitrate, ammonium nitrate, ammonium sulfate, anhydrous ammonia, and others; crucial for vegetative growth and yield enhancement.

● Phosphatic Fertilizers: Mono-ammonium phosphate (MAP), di-ammonium phosphate (DAP), single super phosphate (SSP), triple super phosphate (TSP), and others; important for root development and energy processes.

● Potash Fertilizers: Muriate of potash (MoP) and sulfate of potash (SoP); strengthen crop resilience and quality.

● Secondary Macronutrient Fertilizers: Calcium, magnesium, and sulfur fertilizers; address soil deficiencies and productivity.

● Micronutrient Fertilizers: Zinc, manganese, copper, iron, boron, molybdenum, and others; vital for optimal plant health.

● Complex Fertilizers: Included but detailed analysis not specified.

● Straight fertilizers hold roughly 71.0% market share in 2024.

By Product Form:

● Dry: Holds approximately 86.5% market share in 2024; popular due to cost-effectiveness, storage ease, and wide applicability with slow-release properties.

● Liquid: Present in the market; specific share not provided.

By Crop Type:

● Grains and Cereals: Lead with about 52.0% market share in 2024; major consumers include corn, wheat, and barley requiring significant nitrogen, phosphatic, and potash fertilizers.

● Pulses and Oilseeds: Included but specific details not provided.

● Fruits and Vegetables: Included; importance in specialty crop fertilization.

● Flowers and Ornamentals: Included with specific fertilizer requirements.

● Others: Additional crops included.

Regional Insights

The Midwest region dominates the United States fertilizer market due to extensive cultivation of grains and oilseeds such as corn and soybeans, driving high fertilizer demand. Nitrogenous fertilizers are predominant here, supporting cereal growth, while potash and phosphate fertilizers enhance crop quality and yield. Precision agriculture is widely adopted to optimize nutrient management. This region's leadership in row crop production secures its position as the largest fertilizer consumer in the country.

Speak to An Analyst: https://www.imarcgroup.com/request?type=report&id=19951&flag=C

Recent Developments & News

In January 2025, Michigan Potash secured a USD 1.26 billion loan from the U.S. Department of Energy to boost domestic natural fertilizer production. September 2024 saw Itafos expand into the Brazil market by opening an office in Bahia, contributing 20% of sales expected to rise to 30% by end of 2025. Also in September 2024, AdvanSix received a USD 12 million grant from the U.S. Department of Agriculture to support advanced fertilizer production and strengthen domestic supply chains. In August 2024, Phospholutions partnered with Toros Agri to begin commercial production of its phosphate-based RhizoSorb fertilizer.

Key Players

● CF Industries Holdings, Inc.

● Haifa Group

● ICL Group Ltd

● Koch Industries Inc.

● Nutrien Ltd.

● Sociedad Quimica y Minera de Chile SA

● The Andersons Inc.

● The Mosaic Company

● Wilbur-Ellis Company LLC

● Yara International ASA

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

Tel No: (D) +91 120 433 0800,

United States: +1-201971-6302