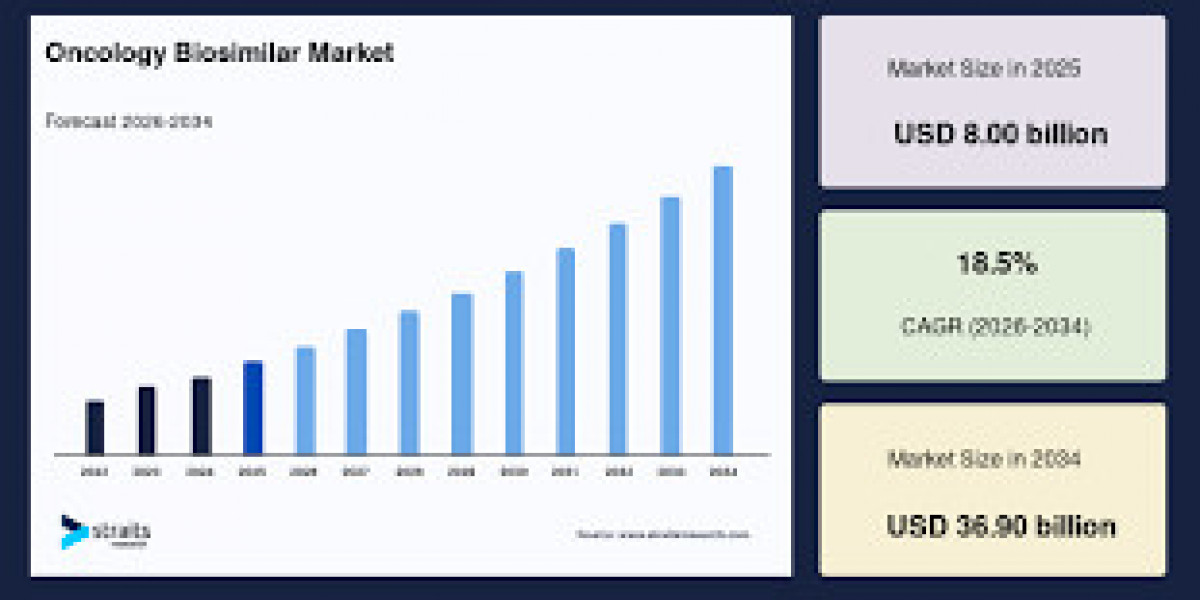

The global Oncology Biosimilar Market is projected to witness robust growth through the forecast period, expanding from an estimated USD 9.48 billion in 2026 to USD 36.90 billion by 2034 at a CAGR of 18.5%. The growth is driven by rising cancer incidence, patent expiries of blockbuster biologics, and increasing adoption of cost-effective biosimilar therapies worldwide.

Key Highlights

Largest Region: North America held the largest share of the oncology biosimilar market in 2025, accounting for approximately 38.14% of total revenue, supported by strong healthcare infrastructure and favorable regulatory policies.

Fastest-Growing Region: Asia Pacific is forecast to be the fastest-growing region, exhibiting a notable CAGR of 19.8%, fueled by expanding healthcare access, growing cancer burden, and local manufacturing growth.

Largest Segment – Product Type: Granulocyte Colony-Stimulating Factor (G-CSF) biosimilars held the largest share in 2025 with approximately 35% market revenue.

Fastest-Growing Distribution Channel: Hospital pharmacies are emerging as a high-growth channel, with a forecasted CAGR of over 18%, driven by centralized procurement and infusion-based oncology care.

Market Dynamics

Drivers:

The oncology biosimilar market is experiencing accelerated adoption due to significant cost advantages over reference biologics, leading to greater healthcare savings and expanded patient access. Biosimilars such as trastuzumab, rituximab, and bevacizumab offer 30–80% cost savings compared to originator drugs, enabling healthcare systems and payers to reallocate resources toward advanced oncology treatments. Regulatory frameworks like the U.S. Biologics Price Competition and Innovation Act and streamlined biosimilar approval pathways have further bolstered market uptake.

Restraints & Opportunities:

Despite growth momentum, market expansion faces headwinds from complex patent litigation and data exclusivity barriers that delay biosimilar launches and limit competitive penetration. However, strategic partnerships, co-development agreements, and portfolio expansion initiatives are creating lucrative opportunities especially in high-value therapeutic segments like immuno-oncology biosimilars. These collaborations are expected to unlock new product pipelines and broaden market reach in emerging and established regions alike.

Explore Market Trends and Forecasts - Download Your Free Sample:

https://straitsresearch.com/report/oncology-biosimilar-market/request-sample

Top Market Players

The global oncology biosimilar landscape features prominent pharmaceutical and biotech firms, including:

Pfizer Inc.

Amgen Inc.

Novartis International AG

Biocon Ltd.

Dr. Reddy’s Laboratories

Samsung Bioepis

Mylan N.V. (now part of Viatris)

Allergan (AbbVie)

STADA Arzneimittel AG

Apotex Inc.

Roche (via biosimilar affiliates)

Sandoz (Novartis division)

Celltrion Inc.

Bio-Thera Solutions

Organon

Teva Pharmaceuticals

Market Segmentation

By Product Type:

Monoclonal Antibodies (mAbs)

Hematopoietic Agents

Granulocyte Colony-Stimulating Factor (G-CSF)

Immunomodulators

By Cancer Type:

Breast Cancer

Lung Cancer

Colorectal Cancer

Cervical Cancer

Blood Cancer / Hematological Cancers

Others

By Route of Administration:

Intravenous (IV)

Subcutaneous (SC)

Others

By Distribution Channel:

Hospital Pharmacies

Retail Pharmacies

Online Pharmacies

Others

By Region:

North America

Europe

Asia Pacific (APAC)

Middle East and Africa (MEA)

Latin America (LATAM)

About the Report

The Oncology Biosimilar Market report provides a comprehensive analysis of industry trends, growth drivers, market dynamics, competitive landscape, and future forecasts through 2034. It includes detailed segmentation by product type, cancer indication, administration route, distribution channel, and regional outlook, offering essential insights for stakeholders, investors, and industry decision-makers seeking strategic guidance in the expanding oncology biosimilar space.