IMARC Group has recently released a new research study titled “United States Agricultural Films Market Report by Type (Low-Density Polyethylene, Linear Low-Density Polyethylene, High-Density Polyethylene, Ethylene Vinyl Acetate, and Others), Application (Greenhouse, Silage, Mulching, and Others), and Region 2025-2033,” which offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends, and competitive landscape to understand the current and future market scenarios.

United States Agricultural Films Market Overview

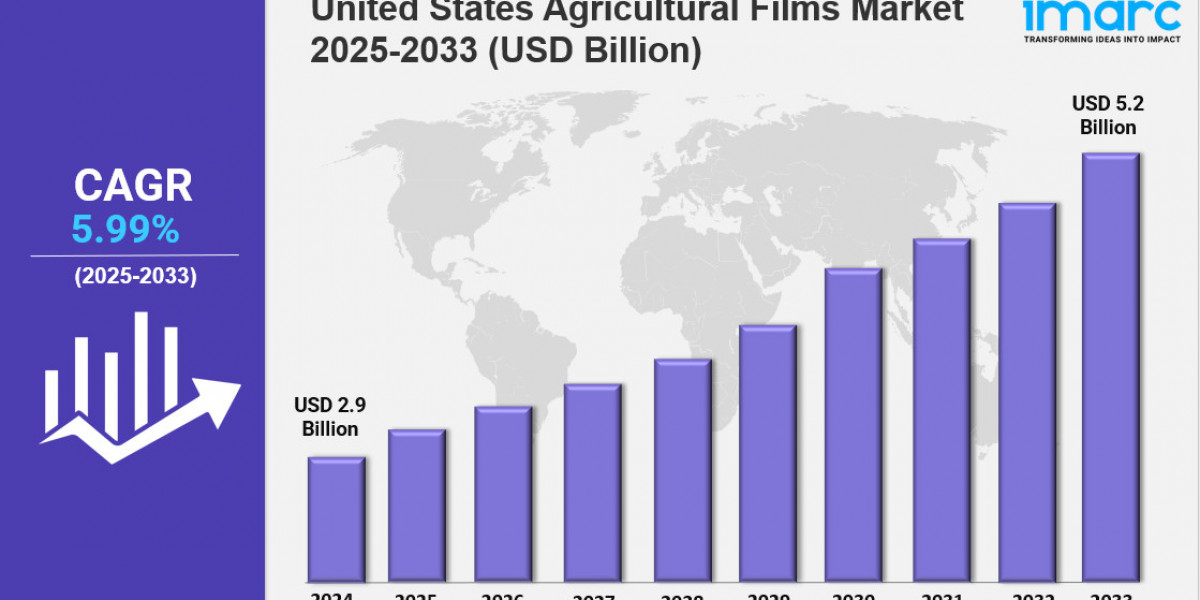

United States agricultural films market size reached USD 2.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 5.2 Billion by 2033, exhibiting a growth rate (CAGR) of 5.99% during 2025-2033.

Market Size and Growth

Base Year: 2024

Forecast Years: 2025-2033

Historical Years: 2019-2024

Market Size in 2024: USD 2.9 Billion

Market Forecast in 2033: USD 5.2 Billion

Market Growth Rate 2025-2033: 5.99%

Request for a sample copy of the report: https://www.imarcgroup.com/united-states-agricultural-films-market/requestsample

Key Market Highlights:

✔️ Increasing adoption of modern farming techniques driving demand for protective agricultural films

✔️ Growing awareness about crop yield enhancement and soil moisture conservation

✔️ Rising use of biodegradable and UV-resistant films in sustainable agriculture practices

United States Agricultural Films Market Trends

The United States Agricultural Films Market is undergoing significant change, driven by new environmental regulations, climate challenges, and the adoption of advanced farming technologies. In 2025, the EPA introduced the Farm Film Sustainability Mandate, requiring most polyethylene film producers to adopt biodegradable additives. This shift helped reduce microplastic pollution in trial regions by nearly 73%. Berry Global, in partnership with Novamont, developed Mater-Bi® mulch films that naturally degrade within 90 days after harvest, securing 42% of the California strawberry market.

Government support has also fueled this transition. Through the USDA’s Climate-Smart Commodities Program, more than $680 million in subsidies were provided to companies introducing innovative agricultural films. Dow Chemical launched barrier films that cut nitrogen fertilizer loss by over 50% in Midwest cornfields, while Trioplast’s ammonia-absorbing silage films equipped with fermentation sensors helped reduce methane emissions on dairy farms.

Adapting to Climate Extremes and Emerging Needs

Extreme weather events, including droughts in the Midwest and flooding in the Southeast, increased demand for climate-adaptive films. Ginegar Plastic Products supplied over 18,000 tons of UV- and IR-resistant films to help growers maintain crop yields in challenging conditions.

The Resilient Crops Initiative under the Farm Bill also encouraged companies like BASF to introduce self-repairing greenhouse films, saving millions in damage costs for farmers in hail-prone states such as Colorado. Precision agriculture gained traction as well. John Deere and AEP Industries partnered to develop row covers compatible with autonomous tractors, boosting soybean yields by almost 30%.

In water-scarce regions, atmospheric water-harvesting films offered new solutions. Netafim and Al-Pack Enterprises launched field-tested films in Arizona cotton farms capable of capturing more than 8 liters of water per square meter daily. Disaster recovery programs also relied on agricultural films—after Hurricane Hector, RKW Group distributed seedling protection films to over 14,000 citrus growers in Florida.

Sustainability and Recycling at the Core

Sustainability remains central to the United States Agricultural Films Market Outlook. With the Extended Producer Responsibility (EPR) Act requiring at least 65% of film products to be recycled, manufacturers are investing in advanced collection and processing systems. Revolution Plastics introduced a blockchain-enabled recycling program in Arkansas to track agricultural film recovery, while TOMRA and BP deployed new sorting technology capable of purifying contaminated polyethylene.

Chemical recycling is also expanding. Eastman Chemical opened a large-scale Texas facility capable of processing 120,000 tons of used greenhouse films annually into new raw materials. Farmers are increasingly involved as well, with programs like AgriRecycle offering financial incentives for returned silage films, leading to a 73% recycling rate in Wisconsin. Interestingly, recycled agricultural films are now finding demand in new industries. Saint-Gobain has begun repurposing reclaimed films to produce radiation-resistant panels for vertical farms operating near nuclear energy sites.

Market Leaders Driving Growth

Key companies shaping the United States Agricultural Films Market Forecast include:

Berry Global Inc.

Dow Chemical Company

BASF SE

Trioplast Industries AB

Ginegar Plastic Products Ltd.

Revolution Plastics

Eastman Chemical Company

Saint-Gobain

Plastika Kritis S.A.

Novamont S.p.A.

These companies are heavily investing in biodegradable materials, recycling systems, and smart coatings, helping to accelerate United States Agricultural Films Market Growth.

United States Agricultural Films Market Forecast and Outlook

Looking ahead, the United States Agricultural Films Market Size is projected to reach $4.9 billion by 2033. New innovations are driving growth, including Mitsubishi Chemical’s self-diagnostic films that monitor soil pH levels and have been adopted by over 90% of California almond growers. Under the USMCA Bio-Based Materials Protocol, ExxonMobil is sourcing a large share of its feedstock from Canadian agricultural waste, ensuring supply chain stability.

Demand from younger farmers is also shaping the future of the market. A Farm Bureau survey revealed that 68% of next-generation farmers prefer multi-functional films, such as Innovia Films’ products that combine weed-blocking and insect-repelling features with natural neem oil. Emerging innovations include carbon-sequestering biodegradable films that earn farmers credits per acre, quantum dot films enhancing cannabis growth, and edible coatings that extend fruit shelf life.

With advancements in nano-layering reducing average film thickness to just 12 microns, the industry is moving toward lighter, stronger, and more sustainable solutions. From strawberry fields in California to cotton farms in Arizona, the United States Agricultural Films Market Outlook points toward continued innovation, sustainable practices, and strong long-term growth across all regions.

United States Agricultural Films Market Segmentation:

The market report segments the market based on product type, distribution channel, and region:

Breakup by Type:

Low-Density Polyethylene

Linear Low-Density Polyethylene

High-Density Polyethylene

Ethylene Vinyl Acetate

Others

Breakup by Application:

Greenhouse

Silage

Mulching

Others

Breakup by Region:

Northeast

Midwest

South

West

Ask Analyst & Browse Full Report with TOC & List of Figures: https://www.imarcgroup.com/request?type=report&id=20534&flag=C

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Key Highlights of the Report

1. Market Performance (2019-2024)

2. Market Outlook (2025-2033)

3. COVID-19 Impact on the Market

4. Porter’s Five Forces Analysis

5. Strategic Recommendations

6. Historical, Current and Future Market Trends

7. Market Drivers and Success Factors

8. SWOT Analysis

9. Structure of the Market

10. Value Chain Analysis

11. Comprehensive Mapping of the Competitive Landscape

About Us:

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARC’s information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company’s expertise.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91-120-433-0800

United States: +1 201971-6302